Official Promissory Note Document for Illinois

Official Promissory Note Document for Illinois

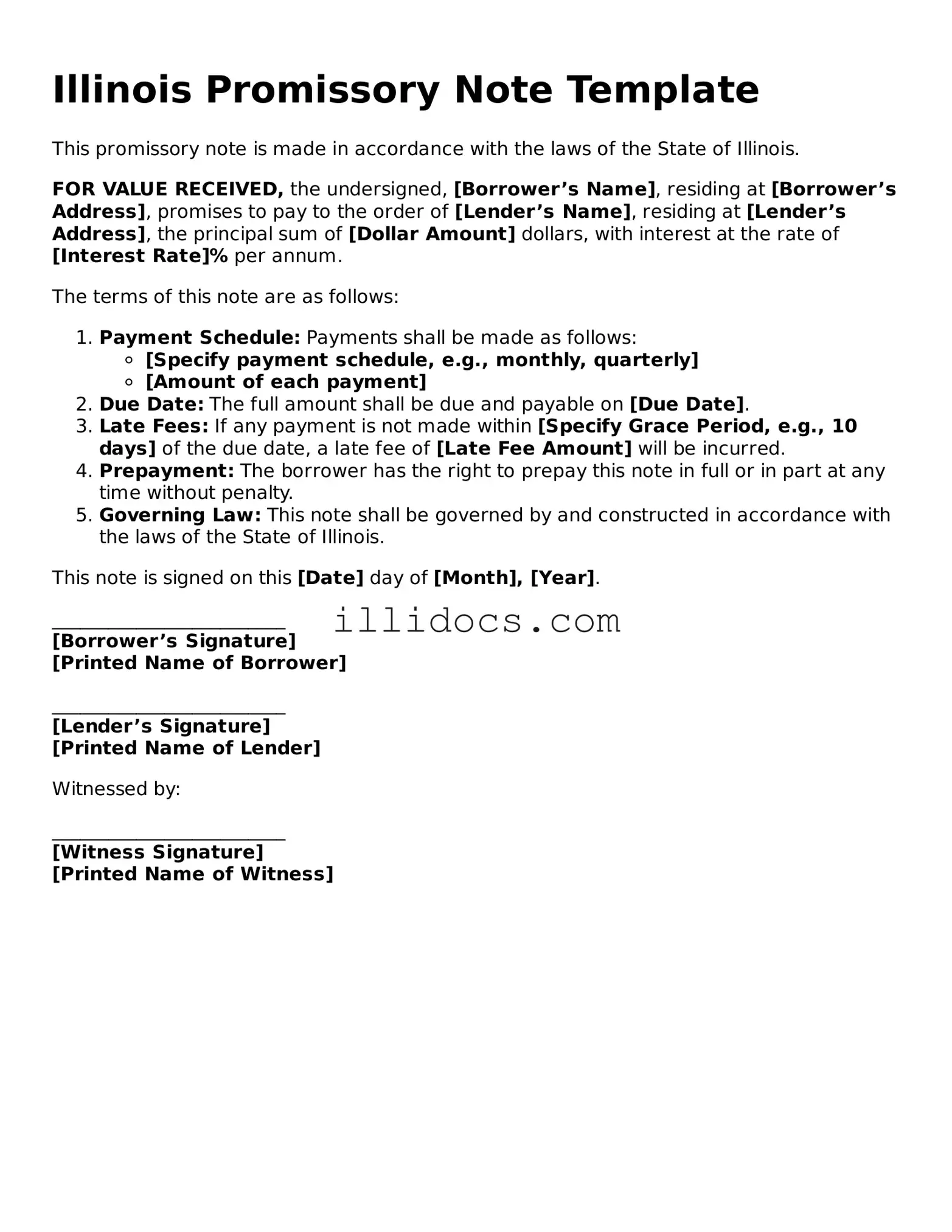

When it comes to borrowing or lending money in Illinois, a Promissory Note serves as a crucial document that outlines the terms of the loan agreement between the parties involved. This written promise details the borrower's commitment to repay the loan amount, specifying the interest rate, repayment schedule, and any collateral involved. It is designed to protect both the lender and the borrower by clearly stating the obligations of each party. Furthermore, the form may include provisions for late fees and default conditions, ensuring that all parties understand the consequences of not adhering to the agreed terms. By formalizing the agreement in writing, the Promissory Note not only provides legal protection but also helps to foster trust between the lender and borrower. Understanding the key components of this document can help individuals navigate their financial agreements with confidence and clarity.

What is a promissory note in Illinois?

A promissory note is a written promise to pay a specific amount of money to a designated person or entity at a particular time or on demand. In Illinois, this document serves as a legal instrument that outlines the terms of the loan, including the principal amount, interest rate, payment schedule, and any consequences for defaulting on the payment. It is a crucial tool for both lenders and borrowers, ensuring clarity and legal protection for both parties involved.

Who can use a promissory note in Illinois?

Any individual or business can use a promissory note in Illinois. Whether you are a private lender offering a loan to a friend or a business providing financing to customers, a promissory note can formalize the agreement. However, it is essential to ensure that both parties understand the terms and conditions outlined in the document to avoid future disputes.

What are the essential elements of an Illinois promissory note?

An effective promissory note in Illinois typically includes several key components: the names and addresses of the borrower and lender, the principal amount being borrowed, the interest rate (if applicable), the repayment schedule, and any penalties for late payments or default. Additionally, signatures from both parties are required to validate the agreement, and it is often advisable to have the document notarized for added legal protection.

Is a promissory note legally binding in Illinois?

Yes, a promissory note is legally binding in Illinois as long as it meets the necessary requirements. Both parties must agree to the terms, and the document must be signed by the borrower. If either party fails to adhere to the terms of the note, the other party has the right to take legal action to enforce the agreement or recover the owed amount.

Can I modify the terms of a promissory note after it has been signed?

Yes, the terms of a promissory note can be modified after it has been signed, but this must be done in writing and agreed upon by both parties. It is crucial to document any changes clearly to avoid confusion or disputes in the future. Both parties should sign the amended document to ensure that it is legally enforceable.

What happens if the borrower defaults on the promissory note?

If the borrower defaults, meaning they fail to make payments as agreed, the lender has several options. They may initiate collection efforts, which can include contacting the borrower for payment or negotiating a new payment plan. If these efforts fail, the lender may choose to pursue legal action to recover the owed amount. Having a well-drafted promissory note can significantly aid in this process.

Do I need a lawyer to create a promissory note in Illinois?

While it is not legally required to have a lawyer draft a promissory note, consulting with a legal professional can provide valuable insights. A lawyer can ensure that the document complies with Illinois law and adequately protects your interests. This is especially important for larger loans or complex agreements.

Are there any specific laws governing promissory notes in Illinois?

Yes, promissory notes in Illinois are governed by both state laws and the Uniform Commercial Code (UCC). The UCC provides a framework for commercial transactions, including the creation and enforcement of promissory notes. It is essential to be aware of these regulations to ensure compliance and protect your rights.

Can a promissory note be used for business loans?

Absolutely. A promissory note is commonly used for business loans. It provides a clear record of the loan agreement between the lender and the business, outlining the repayment terms and any interest charges. This documentation is vital for both parties, as it establishes expectations and legal obligations.

What should I do if I lose my promissory note?

If you lose your promissory note, it is important to act quickly. Notify the other party involved in the agreement and consider drafting a replacement note. It may also be wise to include a clause in the new document stating that the previous note is void. Keeping a copy of the new note and any correspondence related to the lost document is essential for future reference.

Filling out and using the Illinois Promissory Note form can be a straightforward process if you keep a few key points in mind. Here are some important takeaways to consider:

By keeping these points in mind, you can navigate the process of using a promissory note with confidence.

Inaccurate Personal Information: One common mistake is providing incorrect names or addresses. Ensure that all parties' names are spelled correctly and that the addresses are complete.

Missing Dates: Failing to include the date of the agreement can lead to confusion later. Always write the date when the note is signed.

Incorrect Loan Amount: Double-check the loan amount. A simple typo can result in significant misunderstandings down the line.

Omitting Payment Terms: Clearly outline how and when payments will be made. Vague terms can lead to disputes.

Neglecting Interest Rate Details: If there is an interest rate, it must be specified. Leaving this out can create legal challenges.

Not Signing the Document: Both parties must sign the promissory note. Without signatures, the document may not be enforceable.

Ignoring Witnesses or Notarization: Depending on the situation, you might need a witness or a notary. Check the requirements for your specific case.

Failing to Keep Copies: Always make copies of the signed document for all parties involved. This ensures everyone has access to the same information.

Not Reviewing the Document: Before finalizing, take time to review the entire note. Small errors can lead to big problems.

Using Outdated Forms: Make sure you are using the most current version of the Illinois Promissory Note form. Laws and requirements can change.

Once you have the Illinois Promissory Note form in hand, it’s time to fill it out accurately. This process is straightforward, but attention to detail is essential. Make sure to have all necessary information ready before you begin.

After filling out the form, review it carefully to ensure all information is accurate. Both parties should retain copies for their records. This will help prevent any misunderstandings in the future.

Rental Application Form Pdf - State your availability for interviews or further discussions regarding your application.

If you're looking to simplify the process of transferring dirt bike ownership, the vital document for a smooth Dirt Bike Bill of Sale process is essential. It ensures that all pertinent information is included to protect both the buyer and seller during the transaction.

Illinois Promissory Note - Ultimately, clear agreements lead to smoother lending experiences.