Fillable Illinois 700 Template in PDF

Fillable Illinois 700 Template in PDF

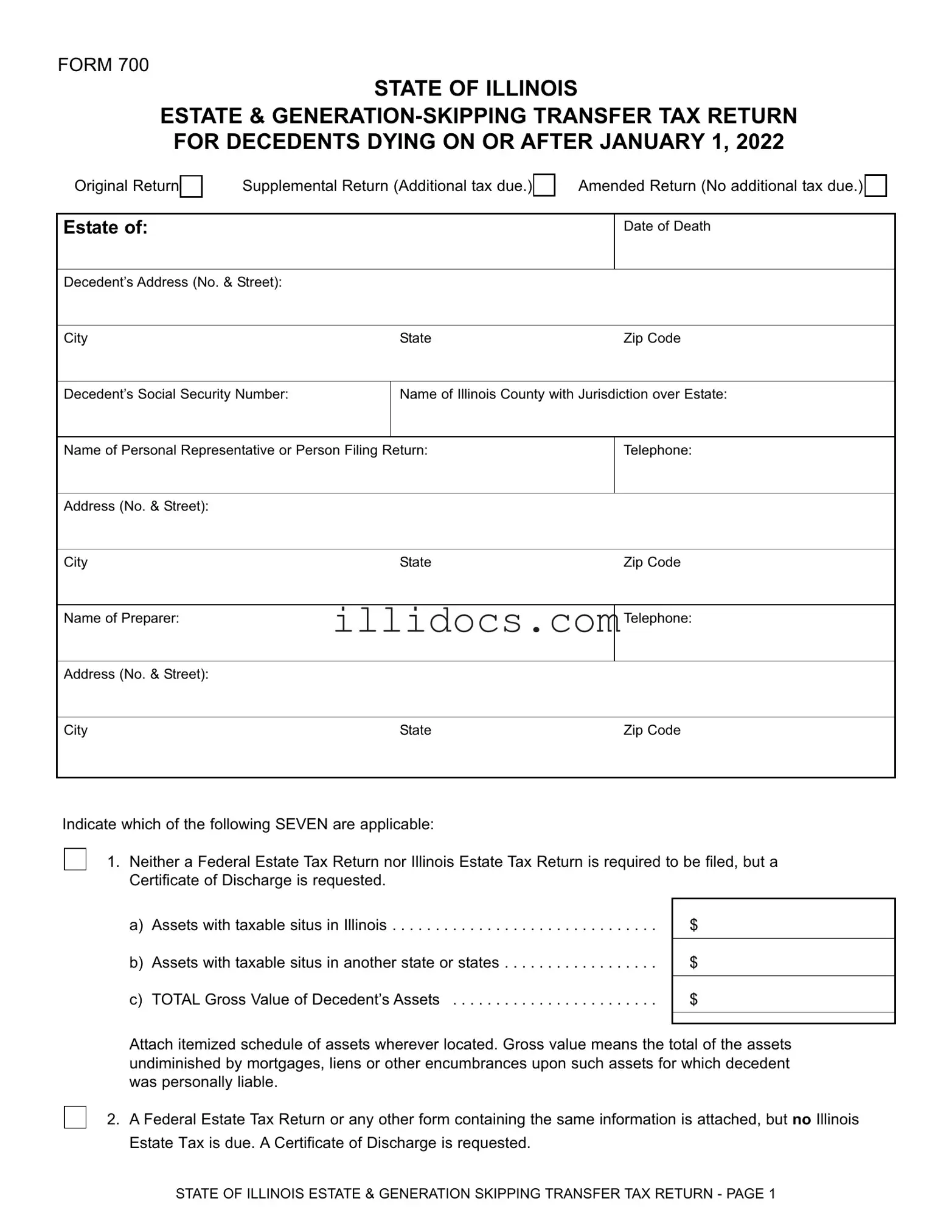

The Illinois Form 700 serves as a crucial document for estates subject to estate and generation-skipping transfer taxes, particularly for decedents who passed away on or after January 1, 2021. This form is essential for estate representatives, as it outlines the necessary information to determine tax liabilities based on the decedent's assets. The form allows for the filing of an original return, a supplemental return for any additional taxes owed, or an amended return if no additional tax is due. It requires details such as the decedent’s date of death, address, and social security number, as well as the name and contact information of the personal representative responsible for filing. Importantly, the form includes options for various scenarios, such as whether a federal estate tax return is attached or if a Certificate of Discharge is requested. Additionally, it addresses the Illinois QTIP election, which can impact the taxable estate, and provides guidance for estates with taxable situs in Illinois. Understanding how to accurately complete this form is vital for compliance and to avoid penalties, as it must be filed within nine months of the decedent’s death. By grasping the major aspects of the Illinois Form 700, estate representatives can navigate the complexities of estate tax obligations more effectively.

What is the Illinois 700 Form?

The Illinois 700 Form is the Estate and Generation-Skipping Transfer Tax Return. It is required for estates of decedents who died on or after January 1, 2021. This form helps determine the Illinois estate tax due based on the decedent's assets and other relevant information.

Who needs to file the Illinois 700 Form?

If the gross value of a decedent's estate exceeds $4 million, the Illinois 700 Form must be filed. This applies regardless of whether a federal estate tax return is necessary. The estate representative is responsible for preparing and submitting this form.

What information is required on the form?

The form requires details such as the decedent's date of death, address, Social Security number, and the name of the personal representative. It also asks for a breakdown of the estate's assets and any applicable elections, like the Illinois QTIP election.

What is the Illinois QTIP election?

The Illinois QTIP election allows the estate to claim qualified terminable interest property for tax purposes. This election can be made in addition to any federal QTIP election. To make this election, specific information must be included on the form, including the dollar amount of the election and the surviving spouse's Social Security number.

How is the Illinois estate tax calculated?

The Illinois estate tax is calculated using a specific formula. The estate representative can use a calculator available on the Illinois Attorney General's website to determine the tax due. This calculation involves the tentative taxable estate and any adjusted taxable gifts.

What happens if the form is filed late?

If the Illinois 700 Form is filed late, penalties may apply. A late filing penalty of 5% of the tax due for each month or portion thereof may be charged, up to a maximum of 25%. Additionally, a late payment penalty and interest may also accrue.

Where should the Illinois 700 Form be filed?

The filing location depends on the decedent's county of residence. For Cook, DuPage, Lake, and McHenry Counties, the form should be filed with the Office of the Attorney General in Chicago. For all other counties, it should be filed in Springfield.

Can I request an extension for filing the form?

An extension can be requested if necessary. This request must be made within nine months of the date of death and should include an explanation or a copy of the federal extension request. The extension applies to both the Illinois 700 Form and any federal estate tax return.

What should I do if I need to amend the form?

If changes are needed after submitting the form, an amended return can be filed. This involves completing the appropriate sections of the Illinois 700 Form and attaching any necessary documentation, such as a copy of the amended federal estate tax return.

Failing to select the correct type of return. Individuals often overlook marking whether the return is original, supplemental, or amended. This can lead to processing delays.

Not providing complete decedent information. Omissions in the decedent’s address, Social Security number, or county can result in the return being rejected.

Incorrectly calculating the gross value of assets. People sometimes misunderstand what constitutes gross value, which should not account for mortgages or liens.

Neglecting to attach necessary schedules. Many filers forget to include the itemized schedule of assets, which is essential for a complete return.

Misunderstanding the QTIP election. Some individuals fail to properly elect for Qualified Terminable Interest Property, including not providing the required social security number of the surviving spouse.

Missing deadlines for filing. The return must be submitted within nine months of the decedent’s death, and extensions require additional documentation that is often overlooked.

Inaccurate calculations of tax due. Errors in the computation of the Illinois estate tax can lead to significant penalties and interest.

Not verifying prior payments. Failing to account for any prior payments can result in overpayment or confusion regarding the balance due.

Ignoring the need for signatures. The return must be signed by both the personal representative and the preparer. Incomplete signatures can cause delays in processing.

Completing the Illinois Form 700 is a critical step in managing the estate of a deceased individual. This form is essential for reporting estate and generation-skipping transfer taxes. Follow these steps carefully to ensure that all required information is accurately provided.

Once the form is filled out, it must be submitted within nine months of the decedent's death to avoid penalties. Ensure that all attachments and supporting documents are included to facilitate the processing of the return.

Illinois Business Address Change - P.O. Box addresses are not acceptable without a physical address accompanying them.

Illinois Power of Attorney for Property 2023 - It's essential to choose an agent whom you completely trust with your medical decisions.